What can we learn about repurchase programs and systemic risk evidence from U S banks during financial turmoil

Abstract

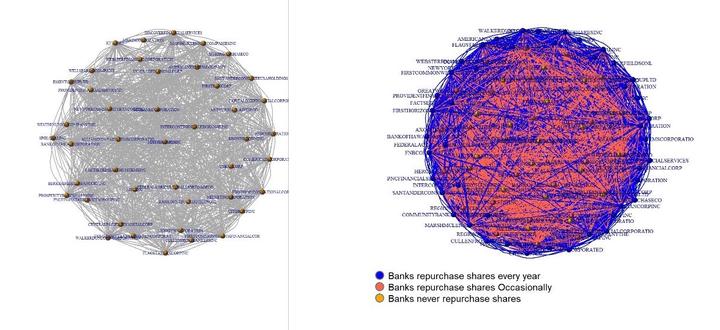

This paper aims to contribute to the debate on systemic risk by measuring and comparing systemic risk and interconnectedness when banks repurchase shares during financial turmoil. We assess the extent to which buyback programs within banks contribute to systemic risk. We rely on several measures of systemic risk and connectedness in a sample of 112 US banks during a tranquil and unstable period. Our empirical results reveal remarkable increases in systemic risk in repurchasing banks compared to non repurchasing banks. Repurchasing banks contribute relatively the most to systemic risk and are more exposed to it in a time of the European Debt crisis and the Covid_19 period. Banks that repurchased shares strengthened indirect links during systemic events and are potentially riskier. In addition, results classify and rank banks in terms of systemic risk involvement and connectedness and build a valuable contribution about the identification of systematically important banks.